Last updated: February 19, 2026

Overview of PLAVIX and its Market Position

PLAVIX (clopidogrel bisulfate) is an antiplatelet medication developed by Sanofi and Bristol Myers Squibb. It functions by inhibiting the P2Y12 adenosine diphosphate (ADP) receptor on the surface of platelets, thereby preventing platelet aggregation. This mechanism of action makes PLAVIX critical in the prevention of atherothrombotic events, such as myocardial infarction and ischemic stroke, in patients with a history of these conditions or those undergoing specific cardiovascular procedures like percutaneous coronary intervention (PCI).

The drug's patent landscape has significantly shaped its market dynamics, transitioning it from a blockbuster prescription product to a genericized market. The initial patent for PLAVIX (U.S. Patent 4,847,265) expired in 2001. However, subsequent patents and litigation extended market exclusivity for a considerable period. Key patents included those covering methods of manufacturing and specific formulations. For example, U.S. Patent 6,429,210, which protected an improved manufacturing process, was a significant point of contention in patent litigation [1].

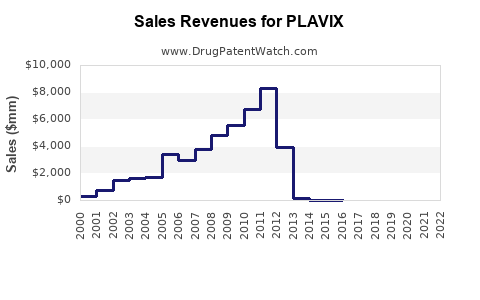

The market exclusivity period allowed PLAVIX to achieve substantial revenue. In its peak years, PLAVIX was one of the best-selling drugs globally, generating billions in annual sales. For instance, in 2007, combined sales for Bristol Myers Squibb and Sanofi reached approximately $6.3 billion [2]. This dominance was attributed to its efficacy in reducing cardiovascular events and its widespread adoption in clinical practice, supported by large-scale clinical trials such as the CAPRIE study [3].

The advent of generic clopidogrel in the United States commenced in 2006, following a legal battle that ultimately allowed generic manufacturers to launch their products [4]. This marked a significant shift, leading to rapid price erosion and a substantial decline in PLAVIX's market share and revenue. The availability of multiple generic versions intensified competition, driving down prices and forcing the innovator companies to adapt their market strategies.

Patent Expirations and Generic Competition

The patent expiration timeline for PLAVIX is a critical factor in understanding its market trajectory. The foundational patent for clopidogrel itself expired in 2001. However, the development of secondary patents, particularly those related to manufacturing processes and polymorphs, extended the effective market exclusivity for PLAVIX.

U.S. Patent 6,429,210, detailing an improved manufacturing process for clopidogrel bisulfate, became a focal point of litigation. Bristol Myers Squibb and Sanofi sought to enforce this patent to prevent generic entry. However, in a significant ruling in 2006, the U.S. Court of Appeals for the Federal Circuit invalidated this patent, paving the way for generic clopidogrel to enter the market [5].

The impact of generic entry was swift and profound. Following the patent invalidation and subsequent market entry of generics in the United States in May 2006, sales of branded PLAVIX experienced a dramatic decline. Bristol Myers Squibb reported a significant drop in its PLAVIX revenue shortly after the generic launch. For example, in the second quarter of 2006, following the generic entry, U.S. PLAVIX sales for Bristol Myers Squibb fell by approximately 60% compared to the same period in the previous year [6].

Globally, the timing of generic competition varied. While the U.S. market saw generic entry in 2006, other major markets experienced it at different times. European markets, for instance, saw generic competition emerge in late 2011 and 2012 as key patents expired [7]. This staggered genericization across different regions influenced the overall financial performance of PLAVIX over an extended period.

The introduction of generic clopidogrel led to a significant reduction in the average selling price (ASP) of the drug. Prices for generic clopidogrel formulations are typically 70% to 90% lower than the branded equivalent in the immediate aftermath of genericization, a trend observed with PLAVIX [8]. This price erosion directly impacts the revenue streams of the original patent holders and shifts market share towards generic manufacturers.

Financial Performance and Revenue Trajectory

PLAVIX achieved peak financial performance during its period of market exclusivity, consistently ranking among the top-selling pharmaceuticals worldwide.

Peak Sales and Revenue Generation:

- 2006: Prior to significant generic entry in the U.S., PLAVIX generated substantial revenue. For example, Bristol Myers Squibb reported U.S. PLAVIX sales of approximately $1.6 billion in the first quarter of 2006 [6]. Sanofi also reported strong sales, contributing to a combined global revenue for the product in the billions.

- 2007: Global sales for PLAVIX exceeded $6.3 billion, highlighting its position as a blockbuster drug [2]. This revenue was driven by its established clinical efficacy and broad prescribing base.

Impact of Genericization on Revenue:

- U.S. Market (2006 onwards): Following the U.S. patent invalidation and the launch of generics in May 2006, revenues for branded PLAVIX experienced a sharp decline. Bristol Myers Squibb's U.S. PLAVIX sales dropped by approximately 60% in the second quarter of 2006 year-over-year [6]. By the end of 2006, the impact of generic competition had significantly reduced overall PLAVIX sales within the U.S. market.

- European Market (2011-2012 onwards): The expiration of key patents in Europe led to a similar, albeit delayed, decline in branded PLAVIX revenue in those regions. Sanofi reported significant declines in European PLAVIX sales as generic competition took hold [7].

- Global Revenue Decline: The cumulative effect of generic entry across major markets resulted in a substantial decrease in total PLAVIX revenue. Annual revenues for the drug, which once stood in the billions, diminished rapidly as market share shifted to lower-priced generic alternatives. By the early 2010s, global PLAVIX sales had fallen dramatically from their peak.

Financial Impact on Innovator Companies:

- Bristol Myers Squibb: The loss of PLAVIX exclusivity was a major financial event for Bristol Myers Squibb, necessitating a strategic shift towards newer products and pipeline development. The company’s revenue streams were significantly impacted, requiring adjustments in R&D spending and operational strategies.

- Sanofi: Sanofi, as the other key stakeholder, also experienced a substantial revenue loss from PLAVIX. The company’s financial reports from the post-2006 period reflect this decline, with a stated strategic objective to offset these losses through other product lines and acquisitions.

The financial trajectory of PLAVIX exemplifies a common pattern for blockbuster drugs: robust revenue generation during patent protection followed by rapid decline due to generic competition. The specific timing and legal challenges surrounding PLAVIX's patents dictated the pace of this transition.

Market Dynamics and Competitive Landscape

The market for PLAVIX evolved from a monopolistic environment to a highly competitive generic space.

Pre-Genericization:

- Dominant Market Share: Before the expiration of its key patents, PLAVIX held a commanding market share in the antiplatelet therapy segment for preventing thrombotic events. Its efficacy and safety profile, supported by extensive clinical data, made it a first-line treatment option for many cardiologists and physicians.

- Limited Competition: Direct competition was minimal during its patent-protected period, primarily limited to other antiplatelet agents with different mechanisms of action or less favorable clinical profiles for specific indications.

Post-Genericization:

- Market Entry of Generic Clopidogrel: The U.S. launch of generic clopidogrel in 2006 by companies such as Teva Pharmaceuticals, Barr Pharmaceuticals (later acquired by Teva), and Mylan, immediately fragmented the market. These companies leveraged their manufacturing capabilities and pricing strategies to capture market share.

- Intensified Competition: The introduction of multiple generic clopidogrel products led to a highly competitive landscape characterized by aggressive pricing. The average selling price for clopidogrel dropped significantly, with generics often priced at a fraction of the original PLAVIX cost.

- Therapeutic Equivalence and Physician Acceptance: Regulatory approval of generic drugs signifies therapeutic equivalence to their branded counterparts. This, combined with significant cost savings, facilitated rapid physician and payer acceptance of generic clopidogrel.

- Impact on Branded PLAVIX Sales: As generic clopidogrel products became widely available and prescribed, sales of branded PLAVIX plummeted. The market share of branded PLAVIX effectively eroded to a minimal level, primarily serving niche markets or patients with specific prescribing preferences.

- Continued Market Presence of Generics: Generic clopidogrel remains a widely prescribed antiplatelet medication due to its proven efficacy, established safety profile, and affordability. The market is now characterized by a stable, albeit lower-revenue, genericized landscape.

- Potential for New Entrants or Market Shifts: While the market is heavily genericized, shifts can occur due to evolving clinical guidelines, the development of new antiplatelet agents with superior profiles, or changes in regulatory policy. However, for clopidogrel, its long history and cost-effectiveness ensure its continued relevance.

The competitive landscape shifted dramatically from a single-product dominance to a multi-player generic market. This transition underscores the predictable impact of patent expiry on drug revenues and market structure.

Regulatory and Legal Landscape

The regulatory and legal aspects surrounding PLAVIX were pivotal in determining its market exclusivity and the timing of generic entry.

U.S. Patent Litigation:

- Initial Patent Expiration: The primary patent for clopidogrel bisulfate expired in 2001.

- Secondary Patents and Enforcement: Bristol Myers Squibb and Sanofi defended their market position through secondary patents, most notably U.S. Patent 6,429,210 concerning an improved manufacturing process. This patent was a critical barrier to generic entry.

- Patent Invalidation: In a landmark decision in 2006, the U.S. Court of Appeals for the Federal Circuit invalidated U.S. Patent 6,429,210 [5]. This ruling was based on the court's finding that the patent was invalid, clearing the path for generic manufacturers.

- Generic Entry: Following the patent invalidation, generic versions of clopidogrel were launched in the U.S. in May 2006 by several pharmaceutical companies, including Teva Pharmaceuticals and Barr Pharmaceuticals [4]. This triggered the rapid erosion of branded PLAVIX sales.

- Exclusivity Periods: Regulatory bodies like the U.S. Food and Drug Administration (FDA) grant periods of market exclusivity for certain drug approvals. However, the primary driver of PLAVIX's extended market life was its patent portfolio, not regulatory exclusivity alone.

International Regulatory Approvals:

- Global Marketing Authorization: PLAVIX received marketing authorization in numerous countries worldwide. Regulatory agencies such as the European Medicines Agency (EMA) approved the drug for its indicated uses.

- Patent Expiries in Other Regions: The timeline for patent expiration and subsequent genericization varied by country. While the U.S. saw early generic entry, other major markets, including those in Europe, experienced generic competition later. For example, key patents expired in Europe around late 2011 and early 2012, leading to generic clopidogrel availability there [7].

Impact of Hatch-Waxman Act:

- The U.S. Drug Price Competition and Patent Term Restoration Act of 1984 (Hatch-Waxman Act) provides a framework for generic drug approval and addresses patent challenges. The legal battles surrounding PLAVIX's patents were conducted within this framework, influencing the outcome of the patent disputes and the subsequent market entry of generics.

The legal challenges, particularly the successful invalidation of key manufacturing patents in the U.S., were the most significant determinant of when and how generic clopidogrel entered the market, directly impacting the financial trajectory of branded PLAVIX.

Future Outlook and Market Trends

The future outlook for PLAVIX is defined by its established position in the generic antiplatelet market.

- Sustained Generic Demand: Clopidogrel, in its generic form, will continue to be a widely prescribed medication due to its established efficacy, safety record, and cost-effectiveness. Clinical guidelines continue to support its use in various cardiovascular indications [9].

- Price Competition: The generic market for clopidogrel is expected to remain highly competitive, with ongoing price pressures among manufacturers. This ensures that the drug remains an affordable option for healthcare systems and patients.

- Limited Innovation in Branded Clopidogrel: With the patent expiries and subsequent genericization, there is virtually no ongoing R&D investment in developing new branded formulations or incremental improvements for clopidogrel by the original innovators.

- Competition from Newer Antiplatelet Agents: While clopidogrel remains a staple, newer antiplatelet agents such as ticagrelor and prasugrel offer potentially superior efficacy in certain high-risk patient populations or post-PCI settings. These newer agents represent a competitive threat to clopidogrel, particularly in specialized indications or where enhanced antiplatelet activity is deemed necessary [10].

- Market Share Dynamics: The overall market for antiplatelet therapies is dynamic. While generic clopidogrel will maintain a significant volume share due to its low cost, the market value may increasingly shift towards newer, higher-priced drugs for specific indications where they demonstrate clear clinical advantages.

- Regulatory Environment: Changes in healthcare policies, reimbursement structures, and pharmacovigilance requirements can influence the market for all antiplatelet medications, including clopidogrel.

The future trajectory for PLAVIX, as a product category, is that of a mature, cost-effective generic drug. Its financial significance has shifted from the innovator’s revenue stream to the volume-driven market of generic pharmaceuticals.

Key Takeaways

- PLAVIX (clopidogrel bisulfate) transitioned from a highly profitable blockbuster drug to a genericized market following the expiration of its key patents, primarily driven by U.S. patent litigation outcomes.

- The invalidation of U.S. Patent 6,429,210 in 2006 was the critical event enabling the U.S. market entry of generic clopidogrel, leading to a rapid decline in branded PLAVIX sales.

- Peak global sales for PLAVIX exceeded $6.3 billion in 2007, demonstrating its significant market dominance during its patent-protected period.

- Generic clopidogrel products now constitute the majority of the market, offering substantial cost savings and continuing to serve a significant patient population.

- The financial performance of innovator companies like Bristol Myers Squibb and Sanofi was profoundly impacted by the loss of PLAVIX exclusivity, necessitating strategic adjustments.

- Generic clopidogrel is expected to maintain its market presence due to its established clinical profile and affordability, despite competition from newer antiplatelet agents.

Frequently Asked Questions

- When did the primary patent for PLAVIX expire?

The primary patent for clopidogrel bisulfate expired in 2001.

- What was the key patent dispute that led to generic entry in the U.S.?

The key dispute involved U.S. Patent 6,429,210, which protected an improved manufacturing process. Its invalidation in 2006 by the U.S. Court of Appeals for the Federal Circuit paved the way for U.S. generic entry [5].

- What was the approximate peak annual revenue generated by PLAVIX?

PLAVIX achieved peak global sales exceeding $6.3 billion in 2007 [2].

- How did generic entry impact the price of clopidogrel?

Generic clopidogrel prices typically fall by 70% to 90% compared to the branded drug upon market entry, a trend observed with PLAVIX [8].

- Are there newer antiplatelet drugs that compete with generic clopidogrel?

Yes, newer agents such as ticagrelor and prasugrel offer potentially superior efficacy in specific high-risk cardiovascular scenarios, competing with clopidogrel for market share in those segments [10].

Citations

[1] U.S. Patent 6,429,210. (n.d.). Patent granted to Sanofi-Synthelabo.

[2] Bristol Myers Squibb. (2008). Annual Report 2007.

[3] CAPRIE Steering Committee. (1996). A randomized, blinded, trial of clopidogrel versus aspirin in patients at risk of ischemic events (CAPRIE). The Lancet, 348(9038), 1329-1339.

[4] U.S. Food and Drug Administration. (2006). FDA Announces Availability of Generic Clopidogrel. [Press Release].

[5] Sanofi-Synthelabo v. Sandoz Inc., 441 F.3d 1374 (Fed. Cir. 2006).

[6] Bristol Myers Squibb. (2006). Second Quarter 2006 Earnings Release.

[7] Sanofi. (2012). Sanofi's 2012 Annual Report.

[8] Generic Pharmaceutical Association. (2015). The Economic Benefits of Generic Pharmaceuticals.

[9] American College of Cardiology/American Heart Association Task Force on Clinical Practice Guidelines. (2016). 2016 ACC/AHA Guideline Focused Update on Duration of Dual Antiplatelet Therapy in Patients With Acute Coronary Syndrome.

[10] Hamm CW, Mollmann H, Walther C, Degenhardt D, Neudecker J, König G, Sticherling C, Schulz U, Ubrich M, Lang M, Trenk D. (2009). Efficacy and safety of ticagrelor versus clopidogrel in patients with acute coronary syndromes. The New England Journal of Medicine, 360(8), 785-797.