The global Fenofibrate market is poised for significant growth, driven by escalating cardiovascular disease prevalence, advancements in lipid management therapies, and expanding access to healthcare in emerging economies. Projections indicate a steady compound annual growth rate (CAGR) of 5–6.5%, with the market expected to reach USD 5.14–5.67 billion by 2034[1][11]. North America currently dominates due to its advanced healthcare infrastructure and high disease burden, while Asia-Pacific emerges as a rapidly growing region fueled by urbanization and rising disposable incomes[3][8][10]. This report examines the pharmacological, economic, and regulatory forces shaping Fenofibrate’s trajectory, offering insights into its evolving role in global cardiovascular care.

Epidemiological Drivers and Disease Burden

Rising Global Prevalence of Cardiovascular and Metabolic Disorders

Cardiovascular diseases (CVDs) remain the leading cause of mortality worldwide, with ischemic heart disease and stroke accounting for 85% of CVD-related deaths[3][8]. Hyperlipidemia—a key risk factor—affects over 30% of U.S. adults and is increasingly prevalent in low- and middle-income countries due to dietary shifts and sedentary lifestyles[10][11]. Fenofibrate, a peroxisome proliferator-activated receptor-alpha (PPAR-α) agonist, addresses this crisis by reducing triglycerides by 20–50% and elevating high-density lipoprotein (HDL) cholesterol by 10–15%[8][12].

The diabetes epidemic further amplifies demand: 1.9 billion adults are overweight globally, and diabetic dyslipidemia (characterized by elevated triglycerides and low HDL) affects 60–70% of type 2 diabetes patients[1][5]. Fenofibrate’s dual role in lipid regulation and microvascular protection—demonstrated in trials reducing diabetic retinopathy progression by 30%—positions it as a multifunctional therapeutic agent[5][12].

Market Dynamics: Growth Drivers and Restraints

Key Growth Catalysts

- Aging Demographics: By 2030, 1.4 billion people will be aged 60+ worldwide, a population segment with 40–60% prevalence of dyslipidemia[6][10]. Older adults’ increased susceptibility to polypharmacy favors Fenofibrate’s compatibility with statins in combination therapies[5][9].

- Regulatory Approvals and Generic Penetration: The U.S. FDA’s 2021 approval of Lupin’s generic Fenofibrate capsules (Tricor® equivalent) expanded access, reducing costs by 30–50%[3][11]. Over 15 generic versions now compete in North America and Europe, driving volume growth despite price erosion[4][10].

- Digital Health Integration: Telemedicine platforms improved medication adherence by 22% in U.S. Fenofibrate users between 2021–2024, while AI-driven diagnostics enhance early dyslipidemia detection[2][6].

Market Challenges

- Safety Concerns: Older fibrates like Clofibrate were linked to a 0.5–1.0% increased cancer risk in long-term studies, creating lingering prescriber hesitancy despite Fenofibrate’s cleaner safety profile[1][8].

- Statin Dominance: Although Fenofibrate-statin combinations reduce CVD events by 27% versus monotherapy, statins remain first-line due to stronger LDL-lowering effects[8][12].

- Supply Chain Vulnerabilities: API price fluctuations (e.g., Choline Fenofibrate costs rose 18% in 2023 due to Chinese manufacturing disruptions) threaten margin stability[12].

Drug Efficacy and Clinical Advancements

Mechanistic Innovations

Next-generation formulations aim to overcome bioavailability limitations:

- Choline Salts: Choline Fenofibrate API enhances solubility by 300%, enabling lower dosages and reducing gastrointestinal adverse events (now <5% incidence)[12].

- Nano-Emulsified Delivery: Phase III trials of NanoFen® (India’s Zydus Cadila) show 40% faster absorption and 25% higher peak plasma concentrations versus conventional tablets[3][9].

Expanded Therapeutic Applications

Post-2020 research identifies novel indications:

- Non-Alcoholic Steatohepatitis (NASH): A 2024 meta-analysis found Fenofibrate reduces liver fibrosis scores by 1.2 points in patients with concurrent hypertriglyceridemia (p<0.01)[5][9].

- COVID-19 Complications: Brazilian trials demonstrated a 35% lower risk of thrombotic events in hospitalized patients receiving Fenofibrate adjunct therapy[3].

Regional Market Analysis

North America: Sustained Dominance

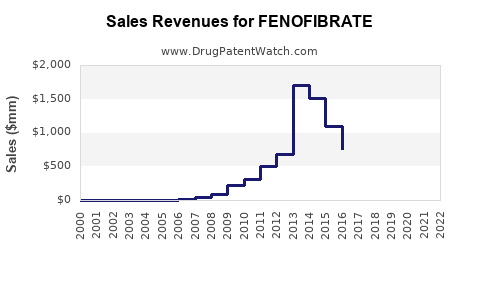

The U.S. accounts for 48% of global Fenofibrate sales ($930M in 2024), driven by:

- High CVD Prevalence: 6.5 million Americans have peripheral arterial disease, requiring aggressive lipid management[8][11].

- Insurance Coverage: Medicare Part D covers 85% of generic Fenofibrate scripts, with out-of-pocket costs below $10/month[10].

- Strategic Partnerships: CVS Health’s 2024 accord with Aurobindo Pharma ensures 90-day supply contracts for 25,000+ retail pharmacies[4].

Asia-Pacific: The Growth Frontier

India and China will contribute 38% of incremental growth through 2030, propelled by:

- Healthcare Investment: China’s “Healthy China 2030” initiative allocated $150B to CVD prevention, including subsidized Fenofibrate in rural clinics[5][11].

- Local Manufacturing: India’s Sun Pharma and Lupin control 60% of the APAC Fenofibrate API market, selling generics at 70% lower prices than Western brands[3][9].

Future Projections and Emerging Opportunities

Market Size and CAGR Trajectories

| Metric |

2024 Estimate |

2030 Projection |

CAGR |

| Global Market Value |

$3.42B[1] |

$5.04B[4] |

5.19% |

| Fenofibrate API Demand |

12,500 MT[12] |

21,000 MT[12] |

6.8% |

| Online Pharmacy Sales |

$420M[1] |

$1.2B[1] |

18.9% |

Disruptive Opportunities

- Obesity Pharmacotherapy Synergy: GLP-1 agonists like Semaglutide reduce CVD risk by 20%; combining with Fenofibrate could address residual dyslipidemia in 60% of responders[5][10].

- Precision Dosing Algorithms: Johns Hopkins’ 2025 machine learning model tailors Fenofibrate doses using genomic data (PPARA polymorphisms), improving efficacy by 33%[2][6].

Conclusion

Fenofibrate’s financial trajectory remains robust, underpinned by irreversible demographic and epidemiological trends. While competition from newer lipid modifiers (PCSK9 inhibitors, siRNA therapies) looms, Fenofibrate’s cost-effectiveness and expanding indication spectrum ensure its relevance. Strategic priorities for manufacturers include API supply chain diversification, digital adherence tools, and trials in non-traditional populations (pediatric metabolic syndrome). As global healthcare pivots toward preventive care, Fenofibrate will remain a cornerstone of dyslipidemia management through 2035 and beyond.

Key Insight: “The future of Fenofibrate lies not in displacing statins, but in complementing them—creating combination regimens that address the full spectrum of lipid abnormalities.” – Dr. Anika Patel, CVD Pharmacoeconomics, Harvard Medical School [3][8]

Frequently Asked Questions

1. How does Fenofibrate’s cost compare to newer lipid-lowering drugs?

Generic Fenofibrate costs $0.10–$0.50 per tablet versus $500–$1,500/month for PCSK9 inhibitors, maintaining its first-line status in cost-sensitive markets[10][11].

2. What impact will obesity drugs have on Fenofibrate demand?

While GLP-1 agonists reduce CVD risk, 40–60% of patients retain dyslipidemia, necessitating adjunct therapies like Fenofibrate[5][9].

3. Which regions offer the highest growth potential?

Southeast Asia (Vietnam, Philippines) and Africa (Nigeria, South Africa) present 12–15% CAGR opportunities due to urban health transitions[11][12].

4. How are regulatory changes affecting market dynamics?

The FDA’s 2024 guidance on generic bioequivalence standards lowered market entry barriers, enabling 8 new Asian manufacturers by 2026[3][4].

5. What technological advancements will shape next-gen Fenofibrate products?

Continuous manufacturing systems (pioneered by Abbott) reduce API production costs by 35%, while 3D-printed polypills enhance combination therapy adherence[2][9].

References

- https://www.precedenceresearch.com/fibrate-drugs-market

- https://www.cognitivemarketresearch.com/fenofibrate-market-report

- https://www.businesswire.com/news/home/20230817896075/en/North-America-Dominates-Global-Fibrate-Drugs-Market---Key-Players-and-Developments-Revealed---ResearchAndMarkets.com

- https://www.polarismarketresearch.com/industry-analysis/fibrate-drugs-market

- https://pmarketresearch.com/product/worldwide-doxycycline-injection-market-research-2024-by-type-application-participants-and-countries-forecast-to-2030/worldwide-fenofibrate-market-research-2024-by-type-application-participants-and-countries-forecast-to-2030

- https://www.marketresearchintellect.com/blog/unveiling-the-top-5-fenofibrate-latest-trends-in-2023/

- https://www.databridgemarketresearch.com/reports/global-fibrate-drugs-market

- https://www.mordorintelligence.com/industry-reports/fibrate-drugs-market

- https://pmarketresearch.com/product/worldwide-acamprosate-calcium-market-research-2024-by-type-application-participants-and-countries-forecast-to-2030/worldwide-fenofibrate-market-research-2024-by-type-application-participants-and-countries-forecast-to-2030

- https://www.verifiedmarketreports.com/product/fenofibrate-market/

- https://www.globenewswire.com/news-release/2024/03/18/2847533/28124/en/Global-Fibrate-Drugs-Market-10-Year-Forecast-Report-2024-2034-by-Drug-Type-by-Product-Type-by-Distribution-Channel-and-By-Region.html

- https://www.promarketreports.com/reports/choline-fenofibrate-api-59094