STRATTERA Drug Patent Profile

✉ Email this page to a colleague

When do Strattera patents expire, and when can generic versions of Strattera launch?

Strattera is a drug marketed by Lilly and is included in one NDA.

The generic ingredient in STRATTERA is atomoxetine hydrochloride. There are sixteen drug master file entries for this compound. Eighteen suppliers are listed for this compound. Additional details are available on the atomoxetine hydrochloride profile page.

DrugPatentWatch® Litigation and Generic Entry Outlook for Strattera

A generic version of STRATTERA was approved as atomoxetine hydrochloride by ZYDUS PHARMS USA INC on September 16th, 2010.

AI Research Assistant

Questions you can ask:

- What is the 5 year forecast for STRATTERA?

- What are the global sales for STRATTERA?

- What is Average Wholesale Price for STRATTERA?

Summary for STRATTERA

| US Patents: | 0 |

| Applicants: | 1 |

| NDAs: | 1 |

| Finished Product Suppliers / Packagers: | 1 |

| Raw Ingredient (Bulk) Api Vendors: | 156 |

| Clinical Trials: | 93 |

| Patent Applications: | 4,009 |

| Drug Prices: | Drug price information for STRATTERA |

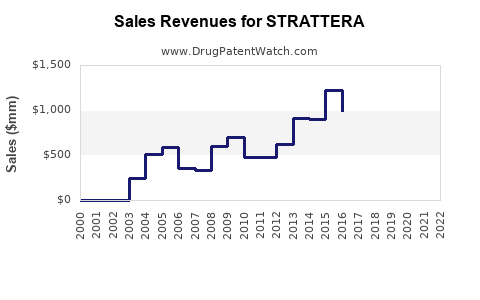

| Drug Sales Revenues: | Drug sales revenues for STRATTERA |

| What excipients (inactive ingredients) are in STRATTERA? | STRATTERA excipients list |

| DailyMed Link: | STRATTERA at DailyMed |

Recent Clinical Trials for STRATTERA

Identify potential brand extensions & 505(b)(2) entrants

| Sponsor | Phase |

|---|---|

| Brown University | Phase 2 |

| National Institute on Alcohol Abuse and Alcoholism (NIAAA) | Phase 2 |

| Takeda Development Center Americas, Inc. | Phase 4 |

Pharmacology for STRATTERA

| Drug Class | Norepinephrine Reuptake Inhibitor |

| Mechanism of Action | Norepinephrine Uptake Inhibitors |

Paragraph IV (Patent) Challenges for STRATTERA

| Tradename | Dosage | Ingredient | Strength | NDA | ANDAs Submitted | Submissiondate |

|---|---|---|---|---|---|---|

| STRATTERA | Capsules | atomoxetine hydrochloride | 10 mg, 18 mg, 25 mg, 40 mg, 60 mg, 80 mg and 100 mg | 021411 | 10 | 2007-05-29 |

US Patents and Regulatory Information for STRATTERA

Showing 1 to 7 of 7 entries

Expired US Patents for STRATTERA

| Applicant | Tradename | Generic Name | Dosage | NDA | Approval Date | Patent No. | Patent Expiration |

|---|---|---|---|---|---|---|---|

| Lilly | STRATTERA | atomoxetine hydrochloride | CAPSULE;ORAL | 021411-007 | Feb 14, 2005 | 5,658,590*PED | ⤷ Try for Free |

| Lilly | STRATTERA | atomoxetine hydrochloride | CAPSULE;ORAL | 021411-003 | Nov 26, 2002 | 5,658,590*PED | ⤷ Try for Free |

| Lilly | STRATTERA | atomoxetine hydrochloride | CAPSULE;ORAL | 021411-004 | Nov 26, 2002 | 5,658,590*PED | ⤷ Try for Free |

| Lilly | STRATTERA | atomoxetine hydrochloride | CAPSULE;ORAL | 021411-001 | Nov 26, 2002 | 5,658,590*PED | ⤷ Try for Free |

| Lilly | STRATTERA | atomoxetine hydrochloride | CAPSULE;ORAL | 021411-008 | Feb 14, 2005 | 5,658,590*PED | ⤷ Try for Free |

| Lilly | STRATTERA | atomoxetine hydrochloride | CAPSULE;ORAL | 021411-006 | Nov 26, 2002 | 5,658,590*PED | ⤷ Try for Free |

| Lilly | STRATTERA | atomoxetine hydrochloride | CAPSULE;ORAL | 021411-005 | Nov 26, 2002 | 5,658,590*PED | ⤷ Try for Free |

| >Applicant | >Tradename | >Generic Name | >Dosage | >NDA | >Approval Date | >Patent No. | >Patent Expiration |

Showing 1 to 7 of 7 entries

International Patents for STRATTERA

See the table below for patents covering STRATTERA around the world.

| Country | Patent Number | Title | Estimated Expiration |

|---|---|---|---|

| Austria | 222757 | ⤷ Try for Free | |

| Canada | 2209735 | TRAITEMENT DE TROUBLE DEFICITAIRE DE L'ATTENTION DE L'HYPERACTIVITE (TREATMENT OF ATTENTION-DEFICIT/HYPERACTIVITY DISORDER) | ⤷ Try for Free |

| Czech Republic | 292226 | Léčivo pro léčení poruchy nedostatku pozornosti/hyperaktivity (Medicament for the treatment of attention deficit/hyperactivity disorder) | ⤷ Try for Free |

| Hungary | 9801283 | ⤷ Try for Free | |

| Luxembourg | 91238 | ⤷ Try for Free | |

| Romania | 118374 | UTILIZAREA TOMOXETINEI IN TRATAMENTUL TULBURARILOR DE TIP HIPERACTIVITATE CU DEFICIT DE ATENTIE (USE OF TOMOXETINE FOR THE TREATMENT OF THE HYPERACTIVITY-TYPE DISORDERS WITH ATTENTION DEFICIT) | ⤷ Try for Free |

| Slovenia | 0721777 | ⤷ Try for Free | |

| >Country | >Patent Number | >Title | >Estimated Expiration |

Showing 1 to 7 of 7 entries

Supplementary Protection Certificates for STRATTERA

| Patent Number | Supplementary Protection Certificate | SPC Country | SPC Expiration | SPC Description |

|---|---|---|---|---|

| 0721777 | 10C0041 | France | ⤷ Try for Free | PRODUCT NAME: ATOMOXETINE OPTIONNELLEMENT SOUS FORME D'UN SEL TEL QUE LE CHLORHYDRATE; NAT. REGISTRATION NO/DATE: NL36369 20100628; FIRST REGISTRATION: GB - PL 00006/0374 20040527 |

| 0721777 | C00721777/01 | Switzerland | ⤷ Try for Free | PRODUCT NAME: ATOMOXETIN; REGISTRATION NUMBER/DATE: SWISSMEDIC 58245 08.04.2009 |

| 0721777 | CA 2006 00030 | Denmark | ⤷ Try for Free | PRODUCT NAME: ATOMOXETIN, EVENTUELT I FORM AF ET SALT DERAF, SASOM HYDROCHLORIDET |

| 0721777 | PA2006006 | Lithuania | ⤷ Try for Free | PRODUCT NAME: ATOMOXETINUM HYDROCHLORICUM; REG. NO/DATE: PL 00006/0374-0379 20040527 |

| 0721777 | PA2006006,C0721777 | Lithuania | ⤷ Try for Free | PRODUCT NAME: ATOMOXETINUM HYDROCHLORICUM; NAT. REGISTRATION NO/DATE: LT/1/06/0431/001-LT/01/06/0431/024 20060621; FIRST REGISTRATION: PL 00006/0374-PL 00006/0379 20040527 |

| 0721777 | SPC/GB04/033 | United Kingdom | ⤷ Try for Free | PRODUCT NAME: ATOMOXETINE, OPTIONALLY IN THE FORM OF A SALT, SUCH AS THE HYDROCHLORIDE; REGISTERED: UK PL 00006/0374 20040527; UK PL 00006/0375 20040527; UK PL 00006/0376 20040527; UK PL 00006/0377 20040527; UK PL 00006/0378 20040527; UK PL 00006/0379 20040527 |

| 0721777 | SZ 18/2006 | Austria | ⤷ Try for Free | PRODUCT NAME: ATOMOXETIN, GEGEBENENFALLS IN FORM EINES SALZES, WIE ALS HYDROCHLORID |

| >Patent Number | >Supplementary Protection Certificate | >SPC Country | >SPC Expiration | >SPC Description |

Showing 1 to 7 of 7 entries

Market Dynamics and Financial Trajectory for Strattera

More… ↓